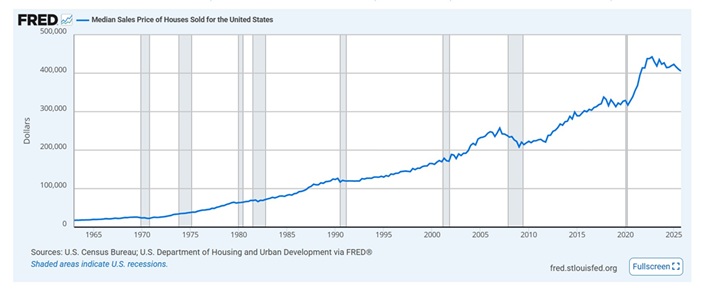

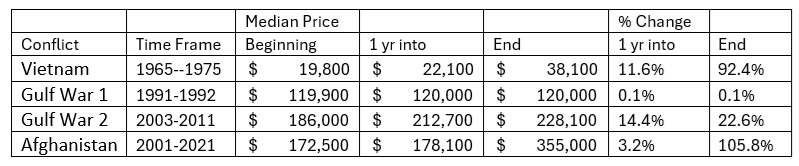

Are San Diego Home Prices Going Up or Down?

Are Home Prices in San Diego Going Up, Down, or Staying the Same?

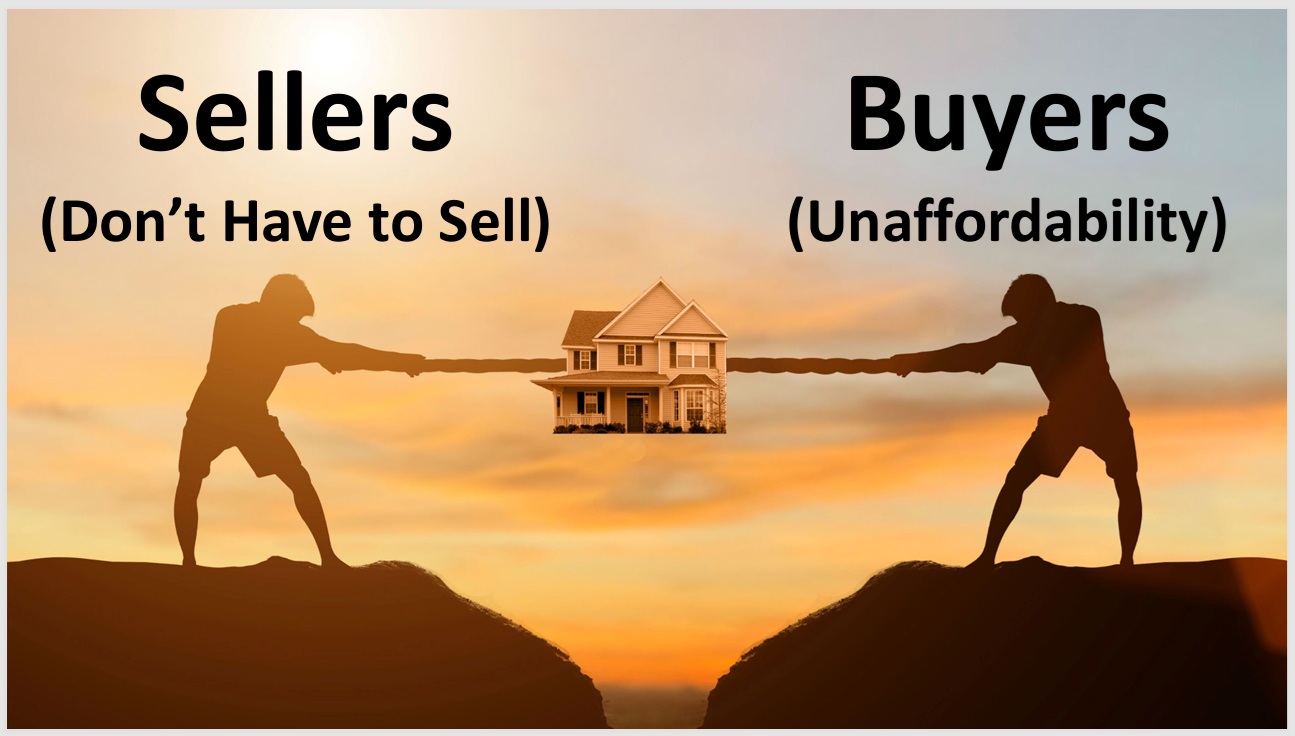

Buy or Sell at the Right Time!

-

Is San Diego a Buyer's Market, a Seller's Market, or a Balanced Market?

-

You'll learn more than just COMPS or an online Zestimate to make an informed decision.

-

What you'll net after all selling expenses

-

Simple Fixups to make $10,000 or more when you sell.

For your free customized report, text your address to George Lorimer at 619-846-1244

What's Your Home Worth?

Cash Offer

You get convenience, certainty, and control.

-

Strong cash offer

-

Sell privately without listing

-

No showings

-

Pick your closing day

-

Cleaning/relocation assistance

-

Rent-back options

On the Market - MLS

You get maximum profit

-

Back-up cash offer

-

Home improvement advances

-

Maximum marketing exposure

-

Expert local market advice

-

Negotiation expertise

June 2026 San Diego Housing UpdateIf you are thinking about buying or selling a San Diego County home in the next 30-60 days, this may be one of the more important market windows of the year. Get your instant home value, request a market value cash offer, search homes, or call/text George directly. With news of an easing Iran conflict and mortgage rates moving lower, some San Diego buyers are wondering if they should wait for even lower rates. That may sound smart, but here is the risk: if rates drop more, buyer competition may increase. That could mean fewer seller concessions, more multiple offers, and higher prices. In other words, the lower rate you are waiting for may come with a higher purchase price. Right now, many San Diego County buyers have more homes to choose from, more negotiating power, and better chances of asking sellers for help with closing costs, repairs, or an interest rate buydown. If rates fall later, you may be able to refinance. But you cannot go back and buy today’s home at today’s price if competition heats up. Many San Diego homeowners are sitting on significant equity. The question is whether that equity is helping you live better, reduce expenses, downsize, buy your next home, invest, or simplify your life. If you are waiting another six months, you may want to ask yourself: what is the real cost of waiting? You could still sell while prices are strong, request a market value cash offer, or use your equity to move into the home or lifestyle you actually want. Online information can only take you so far. Every home, neighborhood, loan, and family situation is different. If you are tired of reading articles, watching videos, and getting generic internet advice, call or text me directly. I will give you specific advice based on your home, your timing, and your goals. George Lorimer Your Home Sold Guaranteed, or I’ll Buy It!* *Conditions apply. Information is intended for general educational purposes only. Your specific buying, selling, financing, tax, and investment situation should be reviewed with the appropriate professionals.

|

Not All The Best San Diego Homes Are Hitting ZillowOff-Market Homes • Coming Soon Listings • Assumable Mortgages Most buyers are still doing the same thing every night: checking Zillow, Redfin, Realtor.com, and hoping something good pops up. The problem is simple. Some of the best San Diego homes never show up where everyone else is looking. Right now, I am seeing homeowners who may sell quietly, investors who would consider an offer before listing, coming-soon properties, and homes with assumable mortgages that most buyers will never find by scrolling online. The biggest mistake buyers are making right now is limiting their search to homes everyone else can see. If you only look online, you are competing with everybody. If you look beyond the public sites, you may find opportunities before the crowd does. Summer in San Diego can create a short window of opportunity. Some sellers want to move before school starts. Some listings have been sitting longer than expected. Some buyers have backed off because of rates. That creates room to negotiate. Text "HIDDEN" to 619-846-1244 I'll send you opportunities that are hard to find on your own, including: Off-Market Homes • Coming Soon Listings • Assumable Mortgages • Seller Credit Opportunities • Price Reductions Start here, or call/text me directly if you want help finding the best opportunities. Call or Text George Lorimer GeorgeLorimer.com

|

What If Waiting to Buy A San Diego home Is Actually Costing You Money?San Diego Housing Update – Summer 2026 George Lorimer | 619-846-1244 See inventory, buyer demand, market time, and pricing trends. Many buyers are waiting for lower mortgage rates. Many sellers are waiting for prices to go even higher. But waiting is not always a strategy. Sometimes it is just fear dressed up as patience. San Diego home prices remain near all-time highs. Over 2,200 homes sold last month. Buyers are still buying. Sellers still have equity. The market is not frozen — people are moving forward. If rates drop, more buyers may jump back in. That usually means more competition, fewer deals, and less negotiating power. Right now, buyers may still be able to negotiate: The smarter move may be buying now, negotiating hard, and refinancing later if rates improve. The question is not just, “What is my home worth?” The better question is: “What is my equity doing for me?” Selling now may allow you to: More homes for sale More negotiating opportunities More seller credits More chances to lower your monthly payment Start with one of the quick links below, or call/text me directly at 619-846-1244. Start your search below, or call/text me at 619-846-1244 if you want help finding the best opportunities. Senior Communities in San Diego If you or a family member is thinking about downsizing, moving to a single-story home, senior community, condo, townhome, or lower-maintenance property, I can help you compare your options. Waiting feels safe, but it may be costing you money, equity, and better choices. Call or Text George Lorimer at 619-846-1244

|

Sold by George Lorimer Rancho BernardoSold for $625,000 3 Beds | 2 Baths | Approx. 1,431 Sq. Ft. | Oaks North 55+ Community Click below to see your cash offer options: Confidential and no-obligation. George Lorimer helped the buyer successfully purchase this Oaks North condo in Rancho Bernardo. This well-maintained 3-bedroom, 2-bath home offered approximately 1,431 square feet, golf course and mountain views, a private balcony, detached garage, guest parking, and low-maintenance 55+ community living. The home featured refreshed flooring, a light neutral interior, ceiling fans, a newer HVAC system, a fireplace in the living room, and one-level living. The community offers access to amenities including pool, spa, pickleball courts, fitness center, clubhouse, and activity spaces. Before you list, you may be able to get a market value cash offer without showings, open houses, repairs, or putting your home publicly for sale. Call or Text George Lorimer at 619-846-1244 25 years of helping clients in Rancho Bernardo and throughout San Diego County. Every home is different. Condition, view, floor plan, upgrades, HOA, location within the community, and current buyer demand all affect value. George can help you compare your options: George Lorimer George Lorimer at ProWest Properties, DRE# 01146839. *Conditions apply.

|

More Homes. More Choices. More Opportunity: San Diego Summer Housing Update 2026Summer is bringing more homes for sale, more negotiating opportunities, and more seller credits across San Diego County. The opportunity: Instead of waiting and hoping rates drop, buyers may be able to use seller credits, closing cost help, or rate buydowns to reduce their monthly payment now. Start your search below, or call/text me directly at 619-846-1244 if you want help finding the best opportunities. Mortgage rates are still one of the biggest challenges for San Diego home buyers. But waiting is not the only strategy. In today’s market, buyers may have more room to negotiate price, closing cost credits, and seller-paid interest rate buydowns. A lot of buyers are sitting on the sidelines waiting for rates to drop. That sounds safe, but there is a risk. If rates drop, more buyers may jump back into the market at the same time. That could mean more competition, fewer deals, and less negotiating power. Right now, some buyers may be able to negotiate: The right home with the right seller credit may save you more than waiting for a small rate drop. Sellers can still do very well in this market, but pricing high and hoping is not a plan. Buyers are comparing your home to every other active listing, price reduction, remodeled home, fixer, and new listing that hits the market. The homes getting the best results usually have: If your home is overpriced or stuck in the “messy middle,” buyers may skip it. That is why it is important to know what your home is really worth before you list. Some of the best opportunities never make it to the MLS. Tell me the neighborhood, price range, and type of home you are looking for. I can help target homeowners in that area to uncover potential sellers before their home is publicly listed. This can be especially helpful if you are looking for: Call or Text George Lorimer 619-846-1244 Your Home Sold Guaranteed, or I’ll Buy It!* *Conditions apply. ProWest Properties. DRE# 01146839.

|

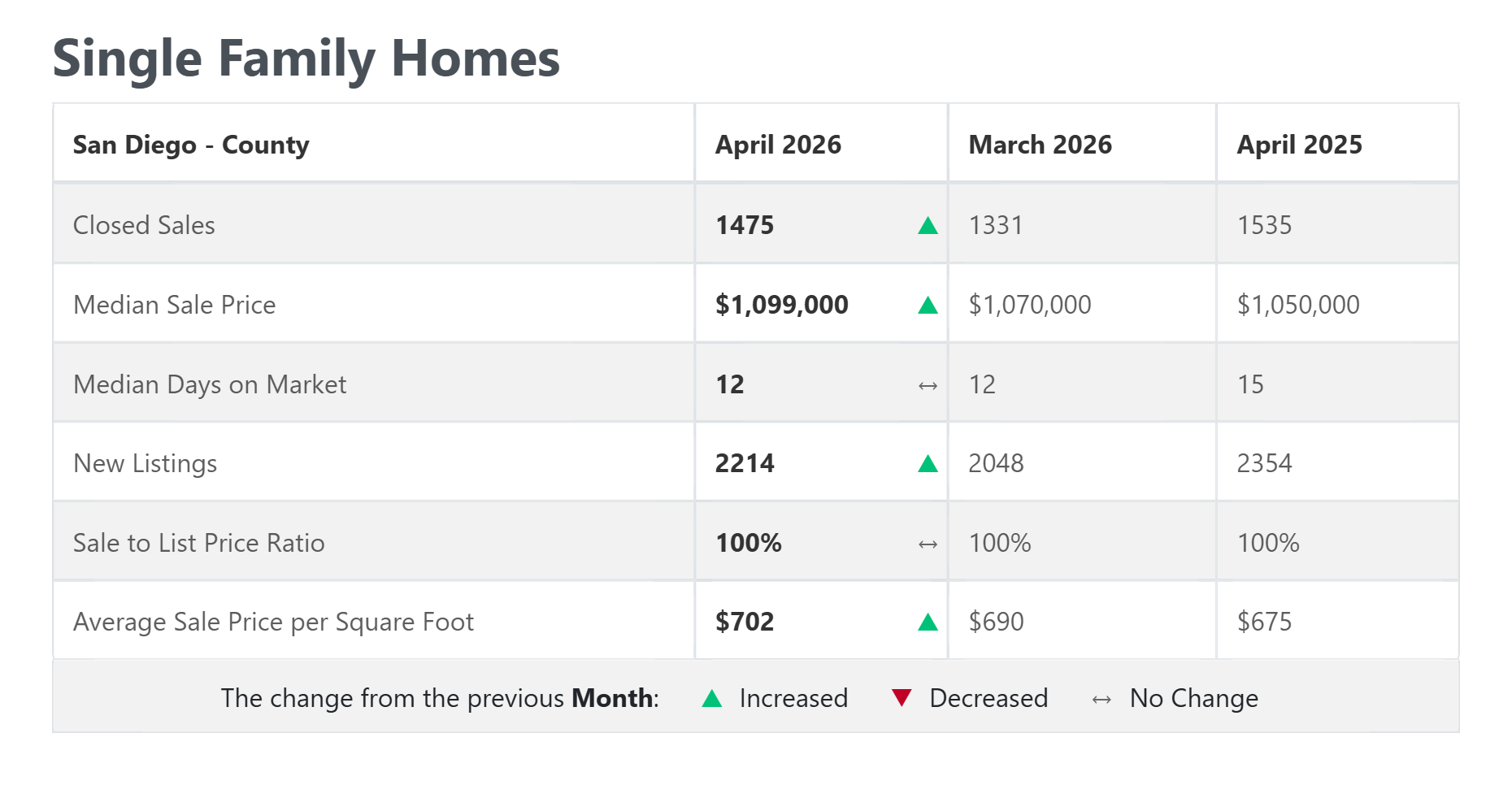

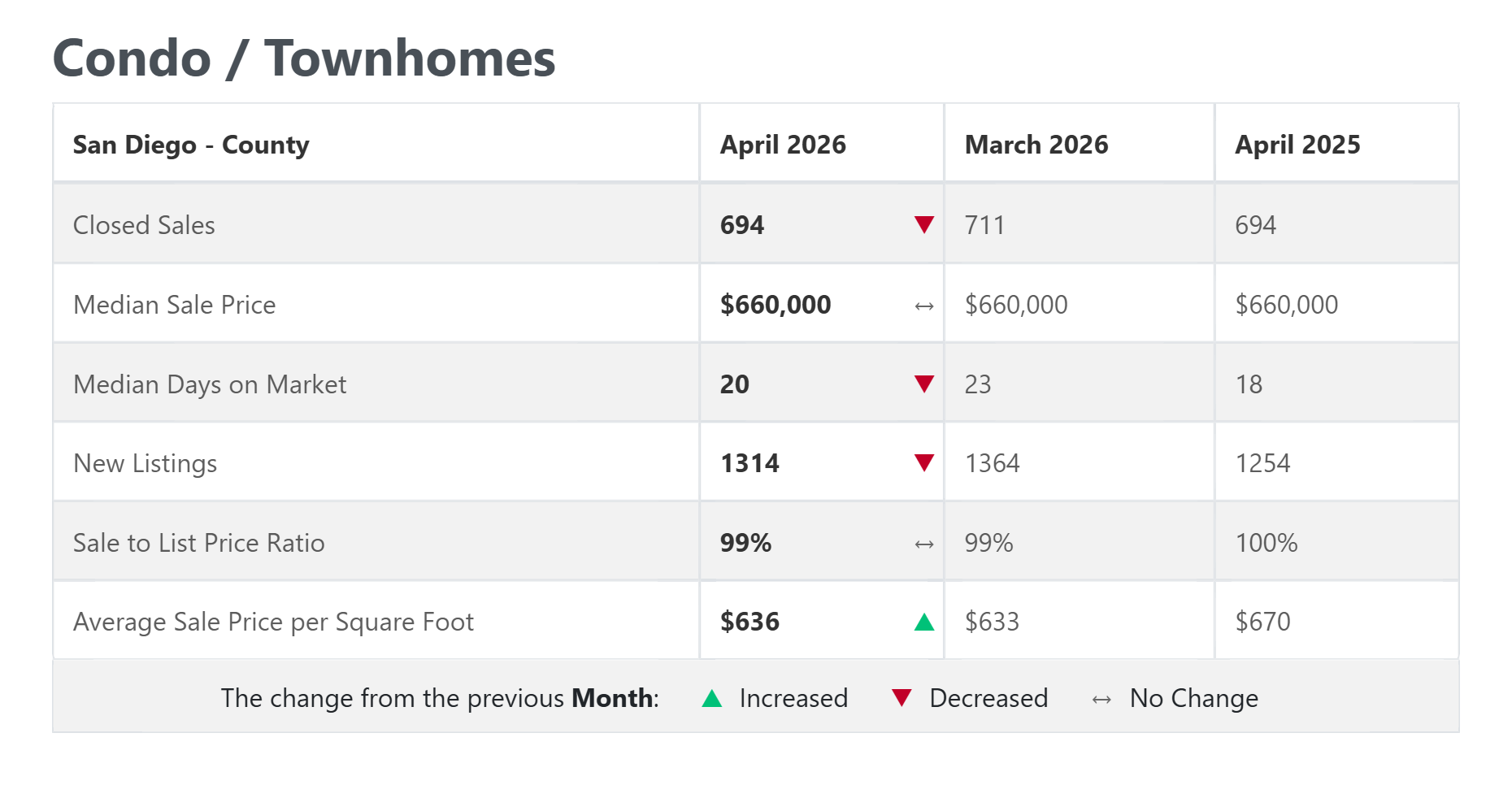

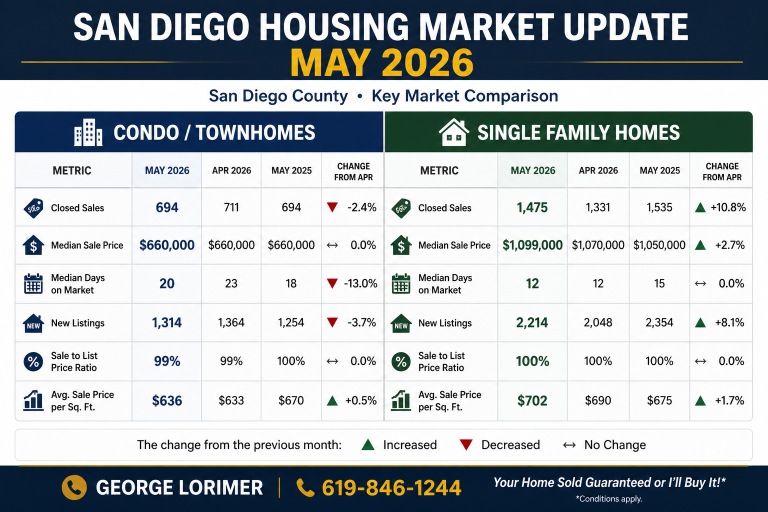

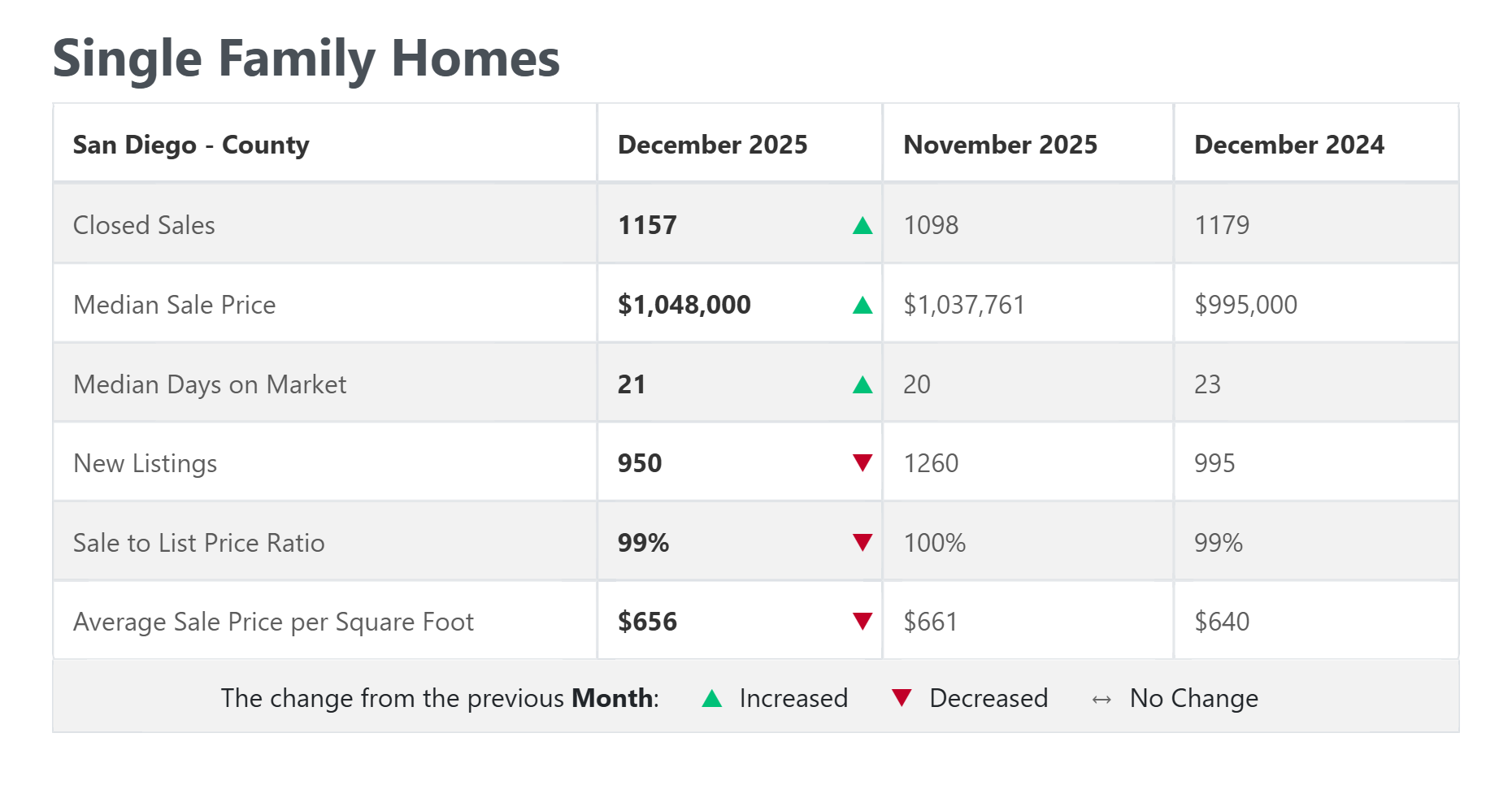

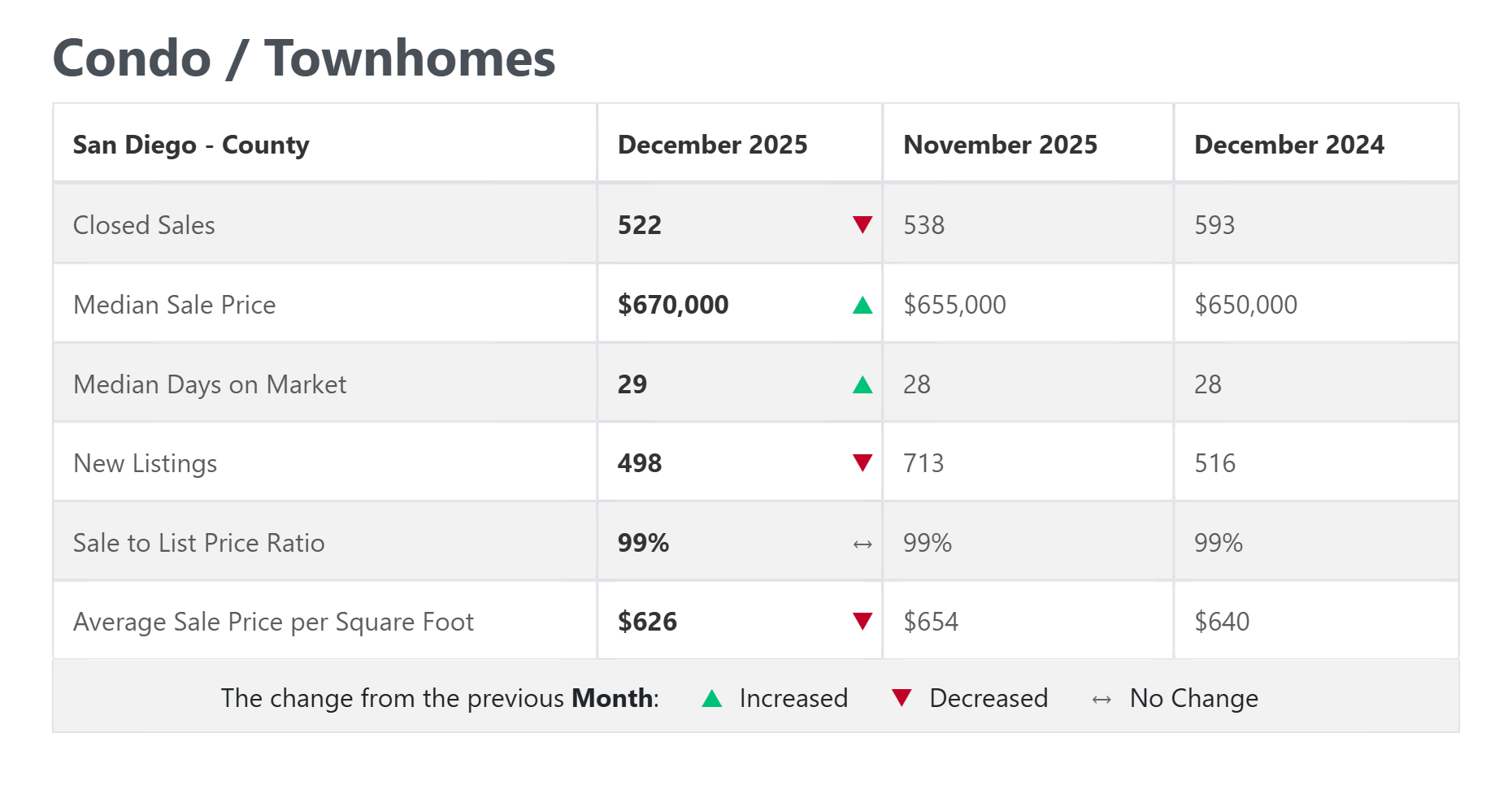

San Diego Housing June 5 2026George Lorimer | 619-846-1244 Skip the endless scrolling. Search homes by area, price, school district, or community. Some of the best opportunities never make it to the MLS. Tell me the neighborhood, price range, and type of home you want, and I can target homeowners directly. Find Unlisted & Off-Market Homes 10247 Caminito Covewood – Scripps Ranch Vaulted ceilings, private deck, treetop views, pool, spa, and a prime Scripps Ranch location. Many San Diego homeowners still have mortgages in the 2% to 3% range that may be assumable by qualified buyers. Search Homes with Assumable Mortgages Detached Homes: Median Price $1,080,000 | 11 Days on Market | 100% Sale-to-List Ratio Condos & Townhomes: Median Price $668,000 | 21 Days on Market | 99% Sale-to-List Ratio For Sellers: Prices remain near record highs, and well-prepared homes are still selling quickly. For Buyers: More inventory and longer market times are creating opportunities to negotiate price, closing costs, and rate buydowns. Call or Text George Lorimer to get started GeorgeLorimer.com

|

Most San Diego Homeowners Don't Realize This Until They Try to Sell

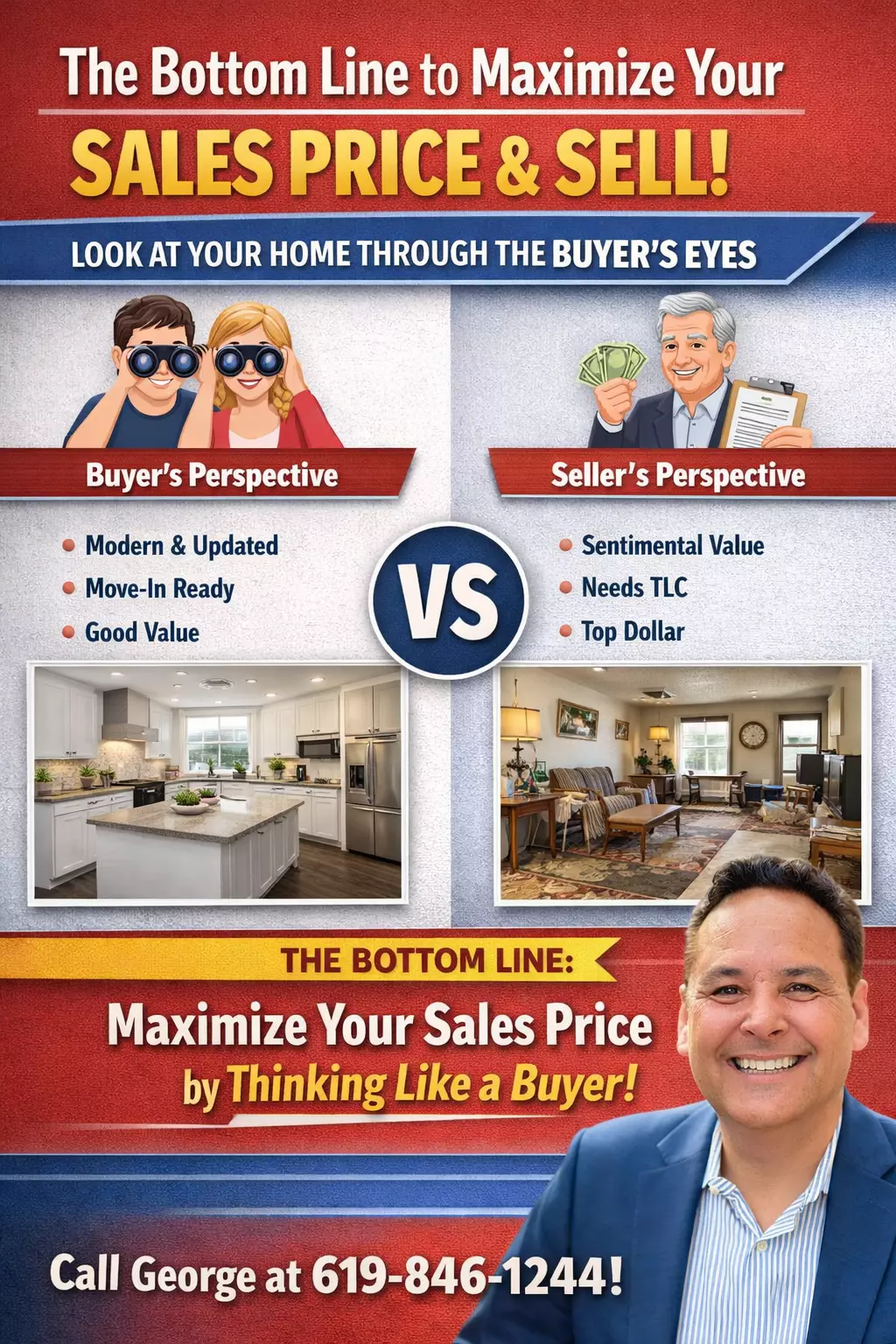

George Lorimer | 619-846-1244 A kitchen remodeled 10 years ago may no longer add much value in today's market. I know that sounds harsh. After helping over 1,000 San Diego families buy and sell homes, this is one of the biggest surprises I'm seeing right now. We're in the middle of our busy late spring and early summer market. In many ways it looks similar to what I've seen over the years, but there are a few trends that are catching homeowners off guard. Here are four things I'm seeing from the front lines of the San Diego housing market. Many homeowners spent good money on improvements 5, 10, or even 15 years ago. The challenge is that today's buyers often view homes in only two categories: There isn't much middle ground. A kitchen remodeled in 2015 may still look great and function perfectly, but many buyers see it as something they'll eventually replace. The result is that some home owners believe should command top dollar are competing against homes buyers consider fixers. The good news? You don't necessarily need a complete remodel. There are a few simple improvements that can dramatically improve buyer perception and help a home avoid the "needs work" category. Many people assume they can simply sell their current home and buy their next one at the same time. It can be done. But it requires planning. What I'm seeing right now is that concurrent closings are difficult and often stressful unless flexibility is built into the transaction from the beginning. The homeowners having the smoothest moves are typically using: A few simple contract terms negotiated upfront can make a huge difference later. Cash offers remain very popular. Many sellers like the convenience of avoiding showings, repairs, open houses, and uncertainty. However, sellers are not willing to give away tens of thousands of dollars simply because an offer is cash. What I'm seeing is that many homeowners will accept a reasonable discount in exchange for convenience and certainty. They just don't want to be taken advantage of. That's why it's important to compare all of your options before accepting an offer. This one surprises sellers all the time. You don't have to fix every issue before selling. But you do need to disclose known problems. And buyers generally don't care whether the issue was your fault, the previous owner's fault, or simply normal wear and tear. What buyers care about is what it will cost them. If the roof is nearing the end of its life, the HVAC system is failing, or there are drainage issues, those costs usually get reflected somewhere in the transaction. The market almost always accounts for deferred maintenance one way or another. The good news is that buyers are still buying. Thousands of San Diego families are purchasing homes every month. Well-prepared homes are still selling quickly. The homeowners who do the best are usually the ones who understand how today's buyers think before they put their home on the market. If you're considering selling in the next 6-12 months, call or text me and I'll send you my free report: "7 Low-Cost Improvements That Help Homes Avoid The Needs Work Category" No obligation. Just practical ideas that can help you maximize your home's value and attract stronger offers. George Lorimer Your Home Sold Guaranteed, or I'll Buy It!*

|

May 28, 2026 San Diego Housing

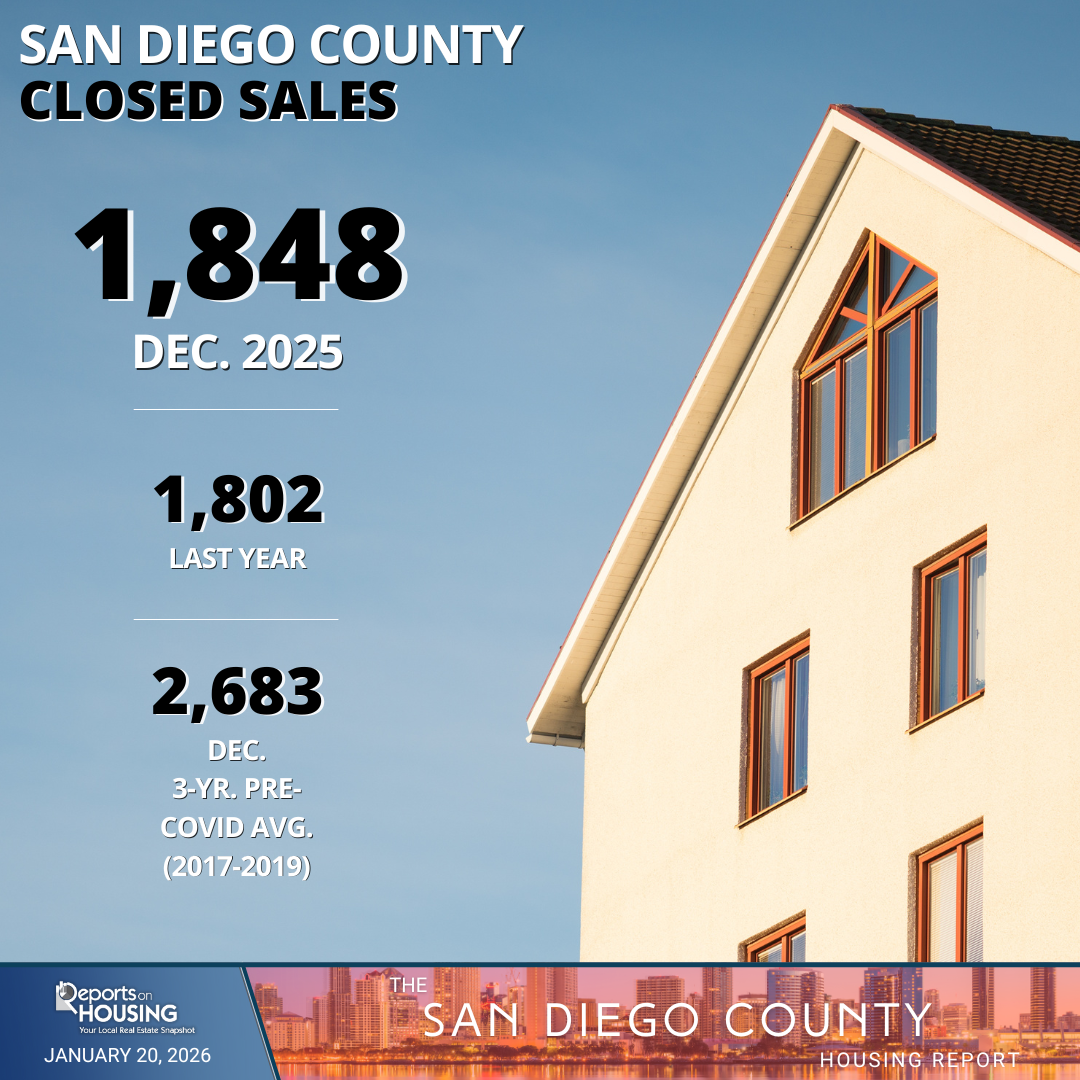

Opportunities for Buyers and Sellers The San Diego housing market is no longer the frenzy we saw during COVID, but it is not a crash either. In many ways, today’s market is creating opportunities for both buyers and sellers — if you understand how to position yourself correctly. Affordability is still the biggest challenge. Higher mortgage rates have slowed demand, buyers are more cautious, and homes are taking longer to sell. But here is the important part: serious buyers are still buying. Over 2,200 San Diegans bought homes last month. That means this is not a dead market. It is a more strategic market. A bright point for sellers is that San Diego home values are still near historic highs in many areas. If you have owned your home for several years, you may still have strong equity. Serious buyers are still out looking, but they are more selective. The homes getting the best results today are properly priced, well presented, professionally marketed, and either move-in ready or strategically refreshed. Many sellers do not need a huge remodel. Often, the best return comes from minimum high-ROI improvements like paint, flooring, lighting, landscaping, cleaning, decluttering, and professional photos. I also offer a Pay-at-Closing option, where many sellers can improve the home with little or no upfront out-of-pocket cost. I help coordinate vendors, and many services can often be paid through escrow at closing. For buyers, today’s market may offer more opportunity than the last few years. More inventory and longer market times can create room to negotiate — especially on homes that have been sitting. Buyers may be able to negotiate a lower price, seller credits, closing cost help, repairs, or even money toward a mortgage rate buydown to lower the monthly payment. In some cases, seller credits can help reduce the payment more effectively than a small price reduction. If you are tired of competing with multiple offers, this market may give you more choices and better negotiating power. This market is not easy for either side, but there are real opportunities. Sellers can still take advantage of historically strong prices. Buyers can take advantage of more inventory, longer market times, and seller flexibility. The key is having the right strategy before you buy, sell, fix up, negotiate, or accept an offer. Call or text George Lorimer for a no-obligation strategy call. George Lorimer

|

Sell As-Is or Fix Up

Get Top Dollar With the Right Strategy Many San Diego homeowners wonder whether they should sell their home as-is or spend money fixing it up first. The mistake is doing nothing when the home needs basic presentation help — or spending way too much on a full remodel that may not pay you back. Most homes do not need a huge remodel. Simple, lower-cost improvements often create the highest return because they help the home look cleaner, brighter, newer, and better in photos. Ballpark estimates for a typical 3BR / 2BA San Diego home around 1,500 SF. Estimated Cost: $4,500–$8,500 Estimated Cost: $9,000–$18,000 Estimated Cost: $1,500–$5,000 Estimated Cost: $2,500–$10,000 Estimated Cost: $800–$3,000 Estimated Cost: $500–$2,500 No Out-of-Pocket Upfront Costs for Many Sellers* I can help coordinate the vendors, prioritize the improvements, and in many cases the vendors can be paid through escrow at closing.* This may include paint, flooring, cleaning, landscaping, minor repairs, decluttering, staging, photos, and marketing. You do not want to overspend. You also do not want to leave money on the table by ignoring simple improvements buyers care about. The right question is not just “Should I fix it up?” The better question is: Which minimum improvements will create the biggest return? Call or text me and I’ll help you compare selling as-is versus doing the minimum high-ROI improvements first. George Lorimer

|

Hot vs Cold San Diego ZIP Codes

George Lorimer at 619-846-1244 Some San Diego homes are still getting multiple offers in under 2 weeks. Others are taking much longer to sell, creating opportunities that buyers may not realize exist right now. The San Diego housing market is no longer “one market.” It depends heavily on the ZIP code, price range, inventory level, condition, and buyer demand in that specific neighborhood. Some areas still favor sellers. Other areas are giving buyers more negotiating room, more choices, and potentially better opportunities. These areas are showing faster days on market, which usually means stronger demand, less buyer leverage, and a better chance for sellers to attract strong offers when the home is priced and presented correctly. For sellers in these areas, the opportunity is to launch correctly. That means strong pricing, professional photos, good presentation, and full market exposure. Even in a stronger ZIP code, overpricing can still kill momentum. These areas are not necessarily “bad” markets. They are areas where homes are taking longer to sell compared to the fastest-moving ZIP codes. That may give buyers more time, more choices, and more room to negotiate. Buyers may have more opportunity in areas with longer market times, especially on homes that are overpriced, need cosmetic work, have been sitting, or have already had price reductions. This is important. A longer average days-on-market number does not automatically mean every home in that area is a bargain. The best homes can still sell quickly. But it does mean buyers should look closely for: Sellers need to be careful. The market is not forgiving overpriced listings the way it did in the past. In strong seller areas, you still need the right launch strategy. In slower areas, pricing, presentation, photos, repairs, and marketing matter even more. Do not assume your home will sell just because San Diego is expensive. Buyers are comparing your home against every other option online. If your price, condition, photos, or presentation are off, buyers notice immediately. I can help you look at your specific ZIP code, price range, and neighborhood to see whether the current market favors buyers, sellers, or is more balanced. If you are buying, I can help you find areas where there may be more negotiating room, including off-market and unlisted homes. If you are selling, I can help you determine the best pricing and presentation strategy before you go on the market. Call or text George Lorimer at 619-846-1244 for a custom buyer or seller strategy. George Lorimer

|

Messy Middle - What is it

George Lorimer at 619-846-1244 Avoid the Messy Middle. This means that your home isn't fully remodeled (within the past 12 months), but you are pricing it the same as that fully remodeled homes. Mortgage rates have pushed back up toward 6.5% as financial markets react to the conflict in Iran and global uncertainty. Higher rates are affecting affordability, slowing parts of the San Diego housing market. But this does not mean the whole market is dead. It means buyers and sellers need to understand which homes are still moving and which homes are getting stuck. If you are buying a home in San Diego, stale listings and longer market times could create real opportunities. Some sellers are now more willing to negotiate than they were a few months ago. The key is knowing which homes are overpriced, which sellers may be flexible, and which homes still require competition. Not every listing is negotiable, but the right stale listing can be a strong opportunity. Sellers should not panic. Buyers are still buying. But buyers today are much more selective. They care about condition, presentation, pricing, photos, flooring, paint, kitchens, baths, lighting, and curb appeal. The homes selling best right now usually fall into two categories. These are the homes with modern flooring, fresh paint, updated kitchens and baths, clean landscaping, strong photos, and the right pricing strategy. These homes can still sell for a premium. A fixer can still sell well if the price makes sense. Buyers will take on work when the value is clear. The problem is when a fixer is priced too close to a remodeled home. The hardest homes to sell right now are the “messy middle” homes. These are homes with older remodels, dated finishes, deferred maintenance, or partial updates, but the seller wants a price similar to the fully remodeled homes. Buyers are not stupid. They compare everything online before they even schedule a showing. If your home needs work, but it is priced like a showcase home, it will sit. Either prepare the home properly so it competes with the best listings, or price it honestly as a home that needs work. Trying to do neither is where sellers lose time and money. For qualified sellers, I can help arrange contractors and front the improvement costs so the home can be prepared properly before going on the market. You can pay for the improvements at closing instead of paying out of pocket upfront. This may include flooring, paint, landscaping, cleaning, lighting, repairs, staging, and other improvements that help the home show better online and in person. San Diego buyers still want homes. Sellers can still get strong results. But the market is less forgiving now. Buyers should look for stale listings where there may be room to negotiate. Sellers should either prepare their home to compete with the best listings or price it correctly for its current condition. If you want real advice based on over 1,000 San Diego home sales, call or text me directly. Call or text George Lorimer at 619-846-1244 George Lorimer, ProWest Properties, DRE# 01146839. Your Home Sold Guaranteed or I’ll Buy It!* *Conditions apply. Information deemed reliable but not guaranteed. Market conditions change quickly. Call George Lorimer at 619-846-1244 for advice specific to your home, neighborhood, and situation.

|

Is that San Diego home Overpriced

George Lorimer at 619-846-1244 Whether you are buying or selling in San Diego, pricing matters. For sellers: the longer a home sits on the market, the lower it usually sells for. For buyers: you do not want to overpay. If a home has been sitting 30–60+ days with no offers and no price reduction, you may have negotiating power and could get a deal. Lots of showings in the first 1–2 weeks? Very few showings? 30 days on market with no offers or reductions? 60+ days on market? Normal price reduction? Email George for a list of San Diego homes with major price reductions, homes sitting 30–60+ days, and possible motivated sellers. george@lorimerteam.com Start with one of these popular San Diego home searches: Call or text George Lorimer for a simple strategy tailored to your home, timing, and goals. George Lorimer | ProWest Properties | DRE# 01146839

|

San Diego Home Buyers in 2026 Are Different, Here’s What Changed

George Lorimer at 619-846-1244 I was showing homes to a young couple in Poway recently when I realized something. They told me they wanted a fixed-up home because they were busy with work and did not have the time — or desire — to renovate a home themselves. That is when it hit me: today’s buyers are different. Years ago, many San Diego buyers were willing to buy a fixer and slowly improve it over time. They wanted to save money and do the paint, flooring, carpet, and updating themselves. Back then, there were not as many remodeled homes or flips competing with regular listings. If a seller simply decluttered, painted, and installed new carpet, the home often stood out. Not anymore. Today, most buyers want the home to already feel done the moment they walk in: updated kitchens, modern bathrooms, fresh paint, new flooring, bright spaces, good photos, and move-in-ready condition. Part of it is lifestyle. People are busier. Many work long hours. And a generation grew up watching HDTV, Flip This House, and beautifully remodeled homes online every day. That quietly changed the San Diego housing market after 2020. Now, turnkey homes often create the strongest buyer urgency and highest offers, while outdated homes tend to sit longer, negotiate more, or require price reductions. This is exactly why many sellers accidentally hurt their sale price. For example, when sellers tell me, “Let’s just give a flooring credit instead of replacing it,” most of the time that does not work nearly as well. Buyers do not emotionally connect with a credit. They connect with what they see the second they walk in. The same thing happens when sellers install the wrong flooring or colors. If buyers today want wide-plank LVP flooring in lighter modern tones that complement the interior paint and overall design, but a seller installs dark carpet or outdated flooring colors, the home usually will not perform nearly as well online or in person. There is a formula to appealing to today’s buyers. All of it works together to create buyer urgency. Many sellers leave money on the table because their home does not create enough urgency online. If you do not have the funds or contractor/vendor contacts, I can help you with the projects, with no payment until we sell your home. It is called my Flip Your Own Home Program. Call or text George to discuss: 619-846-1244. If you only look at fully remodeled homes, you may run into more competition and stronger offers. But many buyers now skip homes that need cosmetic updating. That creates opportunity. The best deals are often homes that need paint, flooring, cleanup, landscaping, or simple updating — not the perfect turnkey homes everyone else wants. Start with one of these popular San Diego home searches: Call or text George Lorimer for a simple strategy tailored to your home, timing, and goals. George Lorimer | ProWest Properties | DRE# 01146839

|

Before you look at San Diego open houses this weekend

George Lorimer at 619-846-1244 Text me your favorite neighborhoods and approximate budget. 619-846-1244 If you’re only waiting for homes to show up on Zillow, Redfin, or Realtor.com, you may already be behind. You know how the process goes. You check the big real estate websites, see a few open houses, drive around all weekend, and get asked the same questions over and over: Then you finally find a home you actually like, and the agent says: “We already have multiple offers.” Current time: 2:45PM. That is why so many buyers get frustrated, stop looking, and then restart the process months later when the same neighborhood may cost tens of thousands more. Instead of waiting for homes to show up online after everyone else already sees them, I help buyers find: I also actively market for homes for my buyers at my own expense. When homeowners raise their hand about possibly selling, my buyers often hear about it before the general public. Online estimates can be useful as a rough starting point, but they often miss the things that actually affect what a buyer will pay: Two homes in the same neighborhood can sell very differently depending on pricing, preparation, marketing, and timing. Get a real-world San Diego home value estimate, not just an online guess. Just text me: I’ll send you both on-market and off-market opportunities that fit what you’re looking for. And in most cases, the seller pays my commission when you buy the home. Call or text me, and I’ll send you new listings plus any off-market homes that fit what you’re looking for. George Lorimer

|

Why some San Diego homes sell in days and others sit

George Lorimer at 619-846-1244 See what buyers would likely pay right now in today’s San Diego market. Others are sitting for months… cutting prices over and over. The market quietly shifted again. Right now, pricing strategy, presentation, photos, marketing exposure, and timing matter more than ever. Many homes that sit too long end up selling for less than they would have if they were priced and launched correctly from the start. Many Zillow and online estimates are missing what buyers are actually paying RIGHT NOW in your neighborhood. George Lorimer | ProWest Properties | DRE# 01146839

|

San Diego Housing Market Just Shifted–How Smart Buyers Are Winning Right Now

George Lorimer at 619-846-1244 San Diego home inventory is up. Rates are still hovering. Buyers are getting more strategic. The people winning right now are not just browsing Zillow. They are using strategies most buyers do not even know exist. Some of the best homes never hit the public sites. That includes off-market opportunities, pre-MLS listings, sellers quietly testing pricing, and homes with possible assumable financing. With prices adjusting and rents staying strong, small multi-unit properties can still be a good long-term play. Yes, they still exist. Some homeowners are locked into ultra-low rates, and in some cases, those loans may be transferable. This can save a buyer hundreds or even thousands per month. They think they have to sell first and risk not finding a home, or buy first and carry two payments. That is outdated thinking. Here is what actually works: I’ll map out your home value, your buying power, and your best strategy. George Lorimer, ProWest Properties

|

San Diego Housing Market Update: Homes Selling Fast, Buyers Gaining PowerGeorge Lorimer at 619-846-1244 San Diego market update — quick and real: Some neighborhoods are as hot as Palm Springs, and others are as cold as La Jolla Cove during May grey. Some observations. You still have leverage right now, but more listings are hitting the market. The longer you wait, the more competition you face. You finally have options again. Less bidding wars, more negotiating power, and better terms. The market has not crashed. It shifted. Targeted marketing, maximum exposure, professional positioning, strong photos, online distribution, buyer follow-up, and a strategy designed to create demand instead of just putting your home online and hoping.

|

San Diego Housing Market Shifting Spring 2026

More homes are hitting the market, buyers are still active, and prices are holding better than expected. Here’s what it means if you’re thinking about buying or selling right now. If you’ve been watching the news, you’ve heard it all: inflation, rates, oil prices, global tension. But here’s what’s actually happening in San Diego right now: the market is adjusting—not crashing. Buyers are still out there and making moves. Homes that are priced right are still going pending in a matter of weeks. Demand didn’t disappear—it paused. This is the biggest shift. More homes are hitting the market, which means more competition. More options for buyers = more competition for sellers. Prices are not crashing. Some areas are slightly down, others stable. This is a balanced market—not a downturn. Waiting hasn’t been helping buyers. You don’t need perfect timing—you need the right strategy. If your home doesn’t fit anymore, this is still a strong window. You have more options than you think. Buy with leverage. Sell with strategy. Use your equity wisely. I’ll help you run real numbers, find opportunities, and build a plan that works.

|

Single Story Temecula Home

|

Why You Dont See All the Available Homes in San Diego Anymore

More listings are being kept exclusive, sold quietly, or shown only on certain platforms. If you are relying on Zillow or Redfin alone, you may be missing homes, better deals, assumable loans, and off-market opportunities. It is getting harder for buyers to see the full picture of what is really available in San Diego. Some homes are being marketed as private exclusives. Some are being kept off the big portals. Others are sold through quiet networks before the public ever gets a fair shot at them. That is a problem if you are trying to buy the right home for the best terms. You need to know about listed homes, off-market homes, assumable loan opportunities, distress sales, price reductions, and sellers willing to negotiate credits or rate buydowns. If you want an edge today, you cannot depend on one website. The buyers getting the best deals are the ones seeing more inventory, acting quickly, and finding homes other people overlook. Sellers are being told that private launches and exclusive exposure create buzz. In a few rare cases, that may make sense for a highly unique luxury property. But for most sellers, less exposure means fewer buyers seeing your home. Fewer buyers usually means less competition. And the longer a home sits on the market, the more buyers expect a discount. If you are planning to buy or sell in the next few months, strategy matters. I will help you sort through what is really available, find the right opportunities, and put together a plan that gets results. With 25+ years of experience and over 1,000 San Diego homes sold, I know how to help buyers and sellers move without wasting time.

|

How Smart Buyers Are Getting Better Deals in San Diego Right Now

|

Is Your San Diego Rental Really Building Wealth

|

San Diego Buyers Just Got More Power (Here’s Why)

Inventory is rising. Buyers have leverage. Sellers still win—but only if priced right. Homes are still selling quickly, but competition is increasing. If you miss your price, you will chase the market down and lose leverage. More listings + longer condo market times = negotiation power. This is where credits, rate buydowns, and deals happen.

|

Price It Right or Overprice? What San Diego Sellers Need to Know

|

Should You Keep Renting… or Buy Before Prices and Payments Move Again in San Diego?

|

Cash Offer or Sell for More? What San Diego Sellers Need to Know First

|

Over 1,000 San Diego Homes Just Hit the Market — Here’s Where the Deals Are

|

Will Iran War Lower San Diego Home Prices

|

San Diego Market Just Shifted: Search Homes, Get Your Value, and See Hard-to-Find Deals

More homes are coming on the market, buyer demand is up, and spring activity is building. That gives buyers more choices right now and gives sellers a chance to sell before more competition shows up. Thinking about buying, selling, or just exploring your options? Use these links first. These are the fastest ways to see what is happening in today’s market and make a smart move. A lot of people are waiting for the “perfect” time. That usually backfires. Buyers may get more competition if rates dip and more people jump in. Sellers may face more competition as more listings hit the market over the next few months. Right now is one of those in-between windows where buyers still have choices and sellers still have leverage. That overlap does not usually last long. You have more choices now than earlier this year, but financing costs already moved up. Waiting could mean a higher monthly payment or more buyer competition later. Buyer demand is stronger than last year, and homes are still selling at about full asking price overall. But more listings are coming, so pricing correctly matters more than ever. Want the deeper numbers, graphs, and local price trends? Download the full market report and review the data for yourself. Do not guess. Get the numbers first. Search homes, get your home value, or look at hard-to-find homes and assumable loan opportunities.

|

San Diego Spring Housing Market Here Early

|

1,009 New San Diego Homes Just Hit the Market — 559 Under $1M

|

san-diego-homes-not-selling-3-reasons

|

San Diego homes hidden inventory

|

San Diego Housing: Buyers Gain $100,000 in Buying Power as Inventory Rises

|

San Diego Market Shift 2026: Buyers Gain Leverage Before Spring Inventory Spikes

|

Are You Living in Your Ideal Home… or Just the Familiar One?

|

San Diego Market Shift: Hot vs Cold Neighborhoods + Your ZIP Code Report

|

San Diego more homes, better deals, see this weekend?

|

What San Diego Housing Slowdown?

|

What Would Have to Happen for San Diego Prices to Crash?

|

Is Your San Diego Neighborhood Hot or Cold in 2026?

|

1,400 Homes Are Selling Every Month in San Diego — Is Yours One of Them?

|

San Diego Homes Are Moving Faster in 2026 (And Here’s Where Demand Is Hottest)

|

Spring Has Already Started in San Diego (Most People Miss This)

|

How do people afford San Diego homes

|

In 2026, Smart San Diegans Don’t Just Look at Prices — They Look at Timing & Options

|

San Diego Real Estate Opportunities Happening Now (Open House + 2–4 Unit Deals)

|

Why 1 in 3 San Diego homes do not sell and what to do about it. Expired listing.

|

San Diego Winter Market Is Here: Prepare for Launch (What Buyers & Sellers Should Do Now)

|

San Diego Housing Market Heating Up This January: Why Smart Buyers and Sellers Are Moving Now

|

Open House Downtown San Diego

|

San Diego Housing Market: Which Neighborhoods Are Hot — and Which Are Cooling in 2026

|

What 6% Rates Mean for Buyers & Sellers

|

2026 San Diego Housing What Buyers and Sellers are Doing

If buying or selling a home in San Diego is even on your radar in 2026, here’s the honest update I’m seeing every day — not the headlines. Buyers want lower mortgage rates, fewer bidding wars, and homes that actually feel like good deals. Sellers want to know if now is the window to sell before more inventory shows up. Here’s the truth: there is no perfect rate and no perfect year. The people who win are the ones who move with a plan — not hope. Online estimates miss what actually drives value in San Diego — condition, layout, upgrades, views, and micro-location. Homes on the same street can vary by hundreds of thousands of dollars. If you want real numbers — or a clear buy or sell plan for 2026 — call or text me directly at 619-846-1244. Helpful resources: P.S. The biggest mistake I’m seeing in 2026 is people waiting for “better conditions” that may never line up. If you want to see what’s actually available right now — including homes not on Zillow — start here before competition picks up.

|

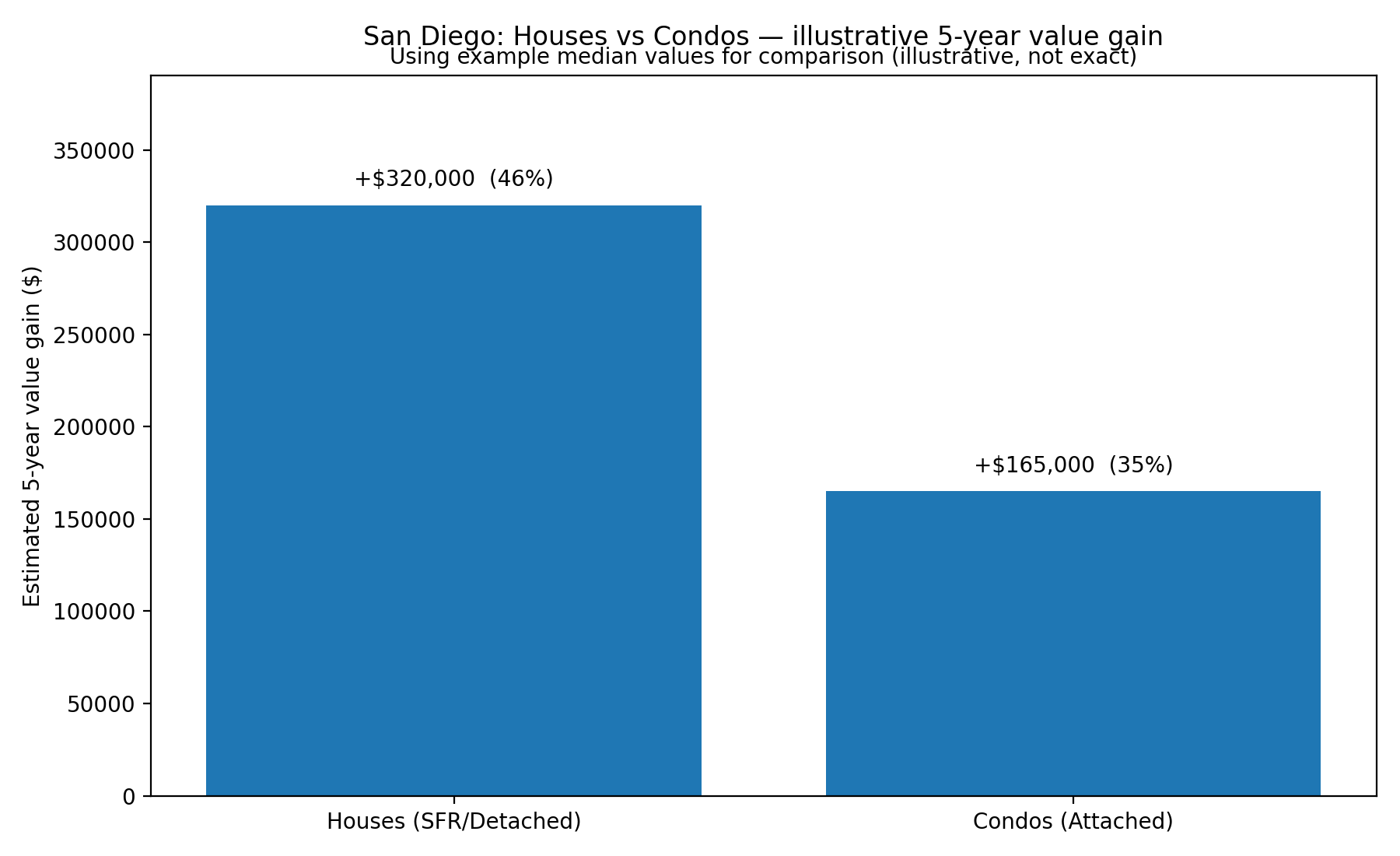

Houses vs. Condos in San Diego: Which Has Been the Better Investment (Last 5 Years)?

|

2026-san-diego-home-buyers-sellers-frustratedBuyers want prices to come down. Sellers want prices to go up. Everyone wants mortgage rates under 6%. Sound familiar? Here’s the part that actually matters: mortgage rates are about 1% lower than last year, and that’s already changing what’s possible—especially for buyers under $1 million. Start here (most popular right now): See what’s available under $1M in San Diego This isn’t headlines or predictions—I’m seeing this daily in real contracts. Some buyers are getting options and leverage again, but only if they know where to look. If selling is even a possibility, the smartest first step is real numbers—not guesses from Zillow. You can see your true value and cash-offer options here: Value and Cash Offers. Waiting for “perfect” usually costs more than moving forward with a plan. If you want help sorting this out quickly, call or text me at 619-846-1244. I’ll give you straight answers and real options. George Lorimer Your Home Sold Guaranteed, or I’ll Buy It* *Conditions apply, ProWest Properties, DRE #01146839?

|

Surprising San Diego Home Trends I See in Person, Not on Zillow

|

2026 San Diego Housing Outlook — What Buyers and Sellers Should Know Now

|

Rancho Peñasquitos & Torrey Highlands Homes 92129 Homes

Fast market snapshot (last 6 months as of Dec 19, 2025). If you want the full spreadsheet (every address + list/sold history), text “92129 DATA” to 619-846-1244. Most Torrey Highlands & newer RP sellers focus here (last 6 months). Want model-by-model detail? Text “92129 DATA” to 619-846-1244. Rancho Peñasquitos overall — sold last 6 months. Thinking of selling? Text your address & timeline to 619-846-1244. Source: SDMLS / ShowingTime ProWest Properties • DRE #01146839 • Your Home Sold Guaranteed or I’ll Buy It* • *Conditions apply I’ve lived and worked in San Diego for over 20 years, helping homeowners make smart decisions about when to sell, when to wait, and how to maximize value without pressure. Real estate is personal — that’s how I treat it. George Lorimer • ProWest Properties • DRE #01146839

|

San Diego home and short sales

|

San Diego’s Best “Quiet Window” to Plan a 2026 Move (Free 10-Minute Strategy Call)

|

How Long Does It Take to Sell a San Diego Home?

If you’re thinking about selling in 2026, here’s the truth: you don’t have to rush out after you sell. You can sell now and move later with a rent-back, or sell very fast if timing matters. Timeline example used below starts January 10, 2026. Your exact timing depends on pricing, condition, neighborhood, and strategy. You get paid first and move later — ideal if you’re finishing the school year or planning a summer move. Single-family homes typically sell faster than condos. Downtown and HOA-heavy condos often take longer, while well-priced houses in strong school districts move quicker. Want a clear plan for your timeline? George Lorimer • ProWest Properties • DRE #01146839

|

Buy a San Diego Home With an Under-6% Mortgage — Guaranteed

The Fed cut rates by 0.25% on December 10, 2025. Good news — but mortgage rates don’t drop automatically. They’re driven by the bond market. The smart move is learning how to secure the lowest rate available right now through negotiation. Call or text 619-846-1244 for a 10-minute strategy call. Want a free, customized report based on your price range and off-market homes? Call or text George at 619-846-1244. 30-year fixed rates are hovering in the low-6% range. FHA and VA can be lower. Sub-6% is achievable when offers are structured correctly. How do you guarantee an under-6% mortgage? I negotiate it with the seller as part of your offer. If they don’t accept it, my lender and I pay the loan discount so you still get the lower rate. Simple — just work with us on your purchase. George Lorimer • 619-846-1244 George Lorimer • ProWest Properties • DRE #01146839

|

San Diego 4-Step Plan to Buy or Sell a Home Without Stress

Most people don’t need more “advice.” They need a simple plan that reduces risk, prevents surprises, and gets them to the finish line. Here’s the exact 4-step process my team uses to help buyers and sellers move fast, stay protected, and avoid drama. Prefer a quick call? Call/Text George Lorimer at 619-846-1244 for a 10-minute strategy session. If the video doesn’t load, view it here: https://www.youtube.com/shorts/AuwjkgTXOxw?feature=share Buyers worry about overpaying or missing out. Sellers worry about pricing wrong, getting lowballed, dealing with repairs and showings, or buying the next home before the current one sells. The solution isn’t hope — it’s a clear process that removes risk. We start with clarity: updated home value, realistic net, buying power, neighborhoods, and what homes are actually available (including unlisted opportunities). This is where you stop spinning and start making smart moves. Most people only see one path: list it and hope, or buy and compete. We lay out multiple paths so you can choose what fits you: cash offer options, multiple investor offers competing, buy-before-you-sell solutions, and the right timing strategy for your goals. Once you choose the best path, my team handles the details: pricing, prep guidance, marketing, negotiation, inspections, and timelines — with one goal: get you the result you want with the least stress and the least wasted time. This is where most agents disappear — and where we do the opposite. We troubleshoot, protect your deal, and keep you informed. If plans change or something comes up, you’ve got an experienced team and real safeguards behind you. Bottom line: I have your back. If you’re thinking about buying or selling in the next 30–90 days, don’t wing it. Get the numbers and your best options first. George Lorimer • ProWest Properties • DRE #01146839

|

Meet George Lorimer San Diego broker and realtor

|

How to avoid the first mistake that San Diego home sellers makeIf you’ve been wondering what's going on in the San Diego housing market, here’s a quick reality check: The reason I tell you this is that there's an opportunity to buy at a good deal in this market. And if you're thinking of selling, don't price your home speculatively. For example, these speculative sellers say things like, "If I could get this price, I'd sell." (usually "their price" is higher than today's market value). For buyers, it becomes clear that the price may or may not have been based on today's statistics. For sellers, it's evident that unless you price it right, you may not sell. Here's my simple 3-step strategy that's helped over 1,000 sellers. 1) Determine that you are committed to selling. 2) Then price your home against competing listings, the homes buyers are comparing yours to. 3) Listen to feedback from the market and buyers and implement changes. Do this right, and you create urgency, competition, and the best chance of selling for top dollar. Call or text me, George, at 619-846-1244 to get your Complimentary Home Seller Report. All the best, George Lorimer Secret selling options that other agents don't offer.

|

San Diego County Housing Report: Go for Gold, No Waiting

|